5 Questions You Should Ask Your Mortgage Lender In This Real Estate Market

A mortgage lender is a bank or company that provides home loans to borrowers. So unless you have $500K lying around, you’ll likely find yourself working alongside a lender during the home-buying process.

A lender will do a thorough review of your spending habits, savings, and credit history. They’ll ask you plenty of thoughtful questions. But, what should you be asking them - especially given today’s real estate market?

Read through this brief list (created by our team of experienced Realtors!) to guide the next conversation that you have with your lender.

1. What is going to impact my monthly payment?

Several factors impact cost. It’s so important to understand which values are fixed. And, how comfortable you will (or won’t) be should your payments slowly increase due to taxes (likely!).

A mortgage payment is made up of these four components:

Principal - the amount that pays down your outstanding loan amount.

Interest - the cost of borrowing money. The amount of interest you pay is determined by your interest rate and your loan balance.

Taxes - the property assessments collected by your local government. Lenders typically collect a portion of these taxes in every mortgage payment and hold the funds in an account, called an escrow account, until they are due.

Insurance - offers financial protection from risk. Like property taxes, homeowners insurance payments are typically held in an escrow account, and then paid on your behalf to the insurance company.

Here’s a breakdown of the monthly mortgage payment for an individual buying in November 2022, in 78724, for $398K:*

Principal & Interest: $2395.25

Property Tax: $596.67

Homeowner's Insurance: $126.32

PMI: $227.37

HOA Fees: $34

Total Monthly: $3,379.61

Cash to Close: $27,757.70

*Example is for a W2 employee, paying $400/month in student loans, with a $300/month car payment, an annual income of $100.8K, and a 720 credit score.

Your lender will better help you understand each of these components of your mortgage, how they change over time, and how they can impact equity.

2. What will this interest rate do to my monthly payment?

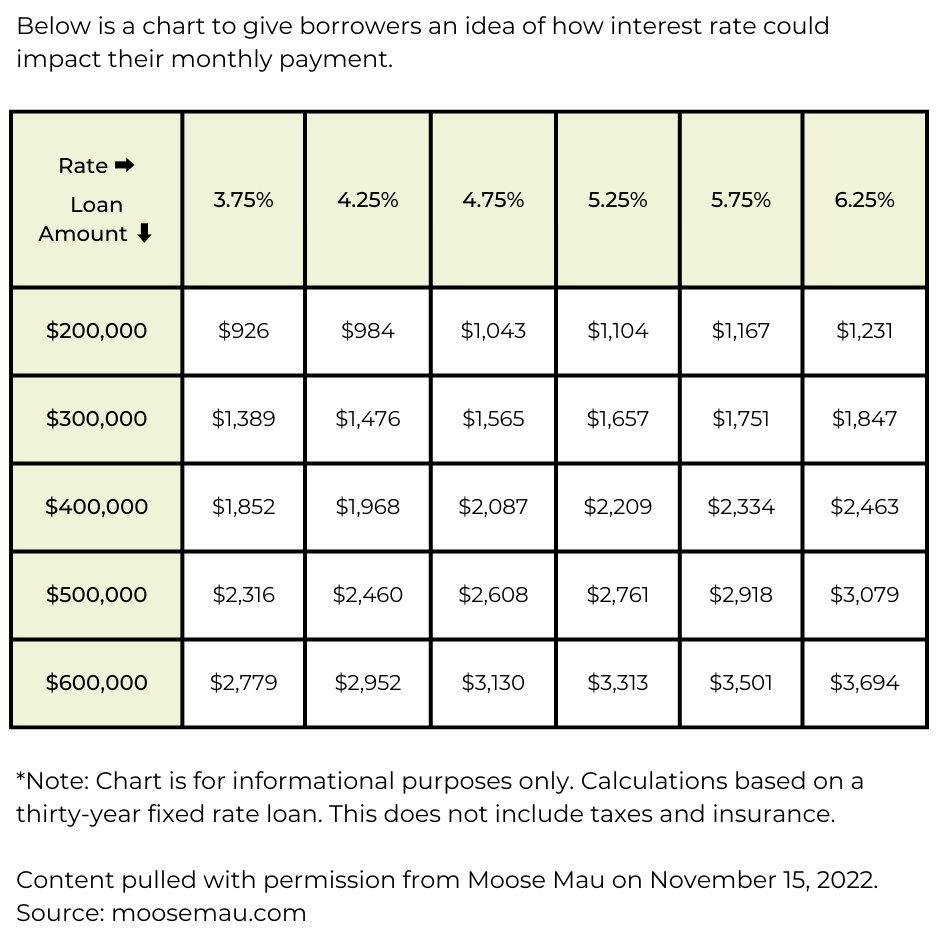

In November, Moose Mau provided these super helpful monthly payment estimations based on interest rates and home prices -

Though, a lender will be able to give an even more exact estimation as they will take into account your unique debt-to-income ratio, salary, credit score, and more.

3. How will property taxes impact my monthly payment?

The tax is determined by multiplying the value of the assessed property by a tax rate, which varies by county or city.

Your city’s assessor(s) and your lender consider the following factors -

Where the property is located

The size of the lot

The size of the house

Current market rates

Grade of the home

Your lender will also look into how taxes were calculated for the previous homeowner. For example, if the house you are looking at is owned by a senior or veteran, then current taxes on the property will not necessarily be the rate you receive - they’d be much lower (Blackhawk Bank).

The right lender will make sure you actually qualify for your mortgage payment based on the correct tax rate.

4. Do you offer a free refinance period? If so, what are the fees associated with that?

Refinancing can allow you to change the terms of your mortgage loan to make it easier to pay your bills or get cash out of your equity.

The costs associated with this usually include an application fee, appraisal fee, attorney fee, title search and insurance. According to RocketMortgage: “Expect to pay around 2-6% of your loan balance in closing costs! You may be able to roll your closing costs into your loan balance, depending on your lender’s requirements.” Note that this is largely impacted by your taxes.

But, what if you could refinance for free? It is an option that some lenders offer - but, you’ll just have to ask to find out.

5. What are my options for rate buy down?

“Rates are too high for me to buy a house!” We’re hearing this all the time - and, that’s fair. But, there are ways to get around this.

Through a buydown, borrowers can obtain a lower interest rate by paying discount points at closing. Discount points, also referred to as mortgage points or prepaid interest points, are a one-time fee paid upfront. In the case of discount points, the interest rate is lower for the loan term.

Example: “If the borrower is obtaining a mortgage for $400,000 and is offered an interest rate of 4%, paying $4,000 would lower their interest rate to 3.75% (Rocket Mortgage).” It may not make sense for buyers to pay for this, but if you can get the seller to do it - you're golden! Since we’re in a buyer’s market, this is way more common.

There are several different types: 1-0 buydown, 2-1 buydown, and 3-2-1 buydown.

Instead of getting in the weeds with us here, we highly recommend having a grade-A lender by your side to educate you on what is best.

If you’re in Austin and want to buy a house within the next year, set up a time to chat with one of our experienced agents. After the call, we follow up with several preferred lender recommendations - folks our clients love working with that can offer competitive rates.

If you’re outside of Austin, we’d be happy to recommend a like-minded Realtor in your city. Just fill out this brief contact form.

For additional real estate market updates and creative home-buying tips, follow us on Instagram and TikTok.

Sources:

Wells Fargo

Blackhawk Bank

The Mortgage Reports

Rocket Mortgage

Bankrate